10 Reasons AI Fails in Insurance (2026)

Why Does AI Keep Failing for Insurers, and How Can You Fix It in 2026?

By Hitul Mistry | April 2, 2026

Editorial Note: This article is written for insurance executives, CTOs, and operations leaders who have invested in AI but are struggling with stalled pilots, poor ROI, or failed deployments. Every statistic cited comes from named 2025 or 2026 industry sources. No fictional case studies are included.

The insurance industry is spending more on AI than ever before. Yet for most carriers, MGAs, and TPAs, the results have been disappointing. Projects stall in pilot. Models produce unreliable outputs. Teams resist new workflows. And after millions in investment, the ROI column stays empty.

This is not an AI problem. It is an execution problem. And it is fixable.

The Numbers Tell a Sobering Story

The gap between AI ambition and AI execution in insurance has never been wider:

- Over 80% of AI projects fail across industries, double the failure rate of non-AI IT efforts (RAND Corporation, 2025)

- Only 22% of insurers who tested AI in 2025 reached full production deployment (All About AI, 2026)

- 42% of companies scrapped most AI initiatives in 2025, up from 17% the prior year (S&P Global, 2025)

- 60% of AI projects unsupported by AI-ready data will be abandoned through 2026 (Gartner, 2025)

- Only 7% of insurers have brought AI to enterprise-wide scale (BCG, 2025)

These are not edge cases. They represent the norm. If your AI initiative is struggling, you are in the majority. The question is what to do about it.

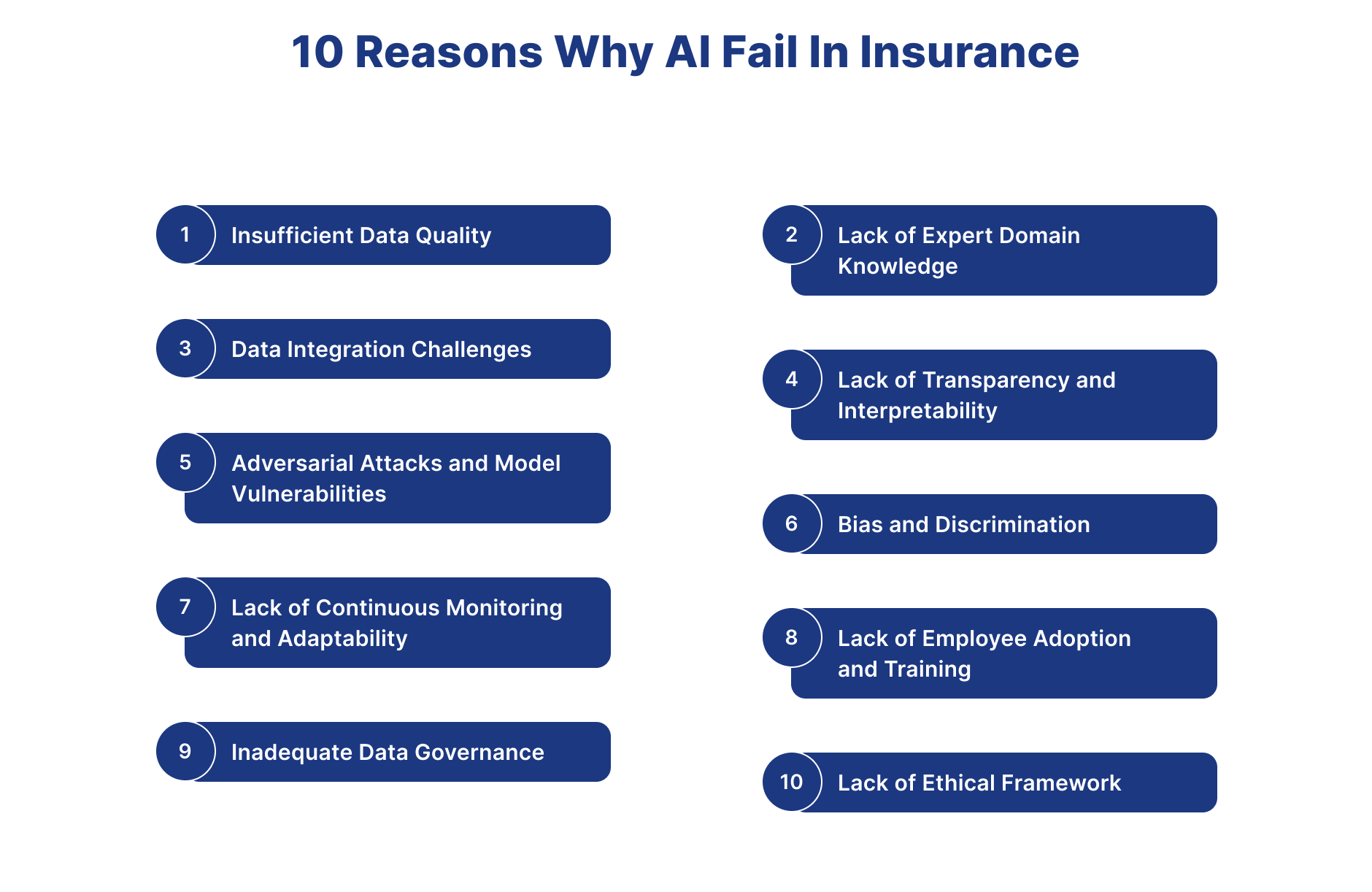

What Are the 10 Hidden Reasons AI Fails in Insurance?

AI fails in insurance not because the technology is immature, but because insurers underestimate the organizational, data, and governance challenges required to make AI work. Below are the 10 most common failure points, each grounded in industry evidence.

1. Poor Data Quality and AI-Readiness Gaps

Insurance data is messy. It lives in legacy policy administration systems, scanned PDFs, handwritten adjuster notes, and inconsistent third-party feeds. According to Gartner, 85% of all AI projects fail due to poor data quality. Furthermore, 78% of organizations cannot validate data before it enters training pipelines (Informatica, 2025).

| Data Problem | Impact on AI | Insurance Example |

|---|---|---|

| Missing fields | Model inaccuracy | Incomplete loss history |

| Inconsistent formats | Pipeline failures | Date formats across systems |

| Duplicate records | Biased training | Same claimant, multiple IDs |

| Stale data | Outdated predictions | Pre-pandemic risk profiles |

When your data is not AI-ready, no amount of model sophistication will compensate. Successful insurers invest in AI-powered document extraction and data normalization before they ever train a model.

2. Lack of Clear Business Objectives

Too many insurance AI projects begin with "let's use AI" rather than "let's solve this specific business problem." Without a defined KPI (such as reducing claims cycle time by 30% or cutting FNOL processing from 48 hours to 4 hours), teams cannot measure success. The project becomes a technology experiment rather than a business initiative.

3. Data Integration Failures Across Siloed Systems

Insurance companies operate dozens of disconnected systems: policy admin, claims management, billing, reinsurance, CRM, and external data vendors. AI models need unified data pipelines that span these systems. When data remains siloed, models see only a fragment of the picture and produce incomplete or misleading outputs.

This is precisely why carriers investing in AI for claims operations must prioritize integration architecture before algorithm selection.

4. The Black Box Problem and Explainability Gaps

Regulators are demanding explainable AI. The NAIC's Model Bulletin on AI Systems requires insurers to demonstrate how AI-driven decisions are made. Colorado's AI Act (SB 24-205), taking effect February 1, 2026, mandates that insurers using AI in high-risk decisions conduct impact assessments and provide consumer disclosures (Fenwick, 2026).

| Regulation | Effective Date | Key Requirement |

|---|---|---|

| Colorado AI Act (SB 24-205) | February 2026 | Impact assessments for high-risk AI |

| NAIC Model Bulletin | Adopted 2023, enforcement ramping | Explainability and bias testing |

| NAIC AI Systems Evaluation Tool | 2026 examinations | AI audit during regulatory exams |

| EU AI Act (extraterritorial) | 2025 onward | Risk classification and transparency |

When underwriters describe AI systems as "black boxes," it signals a governance failure, not a technology limitation. Insurers who invest in AI-driven fraud detection must build explainability into the architecture from day one.

5. Algorithmic Bias and Discrimination Risk

Nearly one-third of health insurers still do not regularly test their AI models for bias or discrimination (IQVIA, 2025). When training data reflects historical underwriting practices that disadvantaged certain populations, AI models can amplify those patterns at scale.

The consequences extend beyond ethics. Biased AI outputs expose insurers to regulatory enforcement, class action litigation, and reputational damage that can take years to repair.

6. Underinvestment in Change Management

McKinsey research indicates that insurers should expect to match their AI development spend dollar-for-dollar with adoption and change management costs. Yet most organizations allocate the vast majority of their budgets to technology and leave pennies for training, communication, and workflow redesign.

The result: expensive AI tools that employees circumvent, ignore, or actively resist.

| With Change Management | Without Change Management |

|---|---|

| 70%+ user adoption within 6 months | Under 20% adoption after 12 months |

| Clear role definitions for AI-human workflow | Confusion and duplication of effort |

| Executive dashboard tracking adoption KPIs | No visibility into utilization |

| Continuous feedback loops for model improvement | Models degrade without user input |

7. Employee Resistance and Skills Gaps

Nearly half of insurance employees surveyed rated their current level of AI support as "moderate or less" (Wolters Kluwer, 2025). There is a measurable gap between the AI support employees want and what they actually receive. Without targeted upskilling programs, your most experienced underwriters and adjusters will revert to manual processes.

Organizations exploring AI agents for cross-selling must recognize that technology adoption depends on the people using it, not just the algorithms powering it.

8. Inadequate Data Governance Frameworks

Data governance is not a one-time project. It is an ongoing discipline that covers data lineage, access controls, quality monitoring, retention policies, and regulatory compliance. Without it, AI models train on corrupt inputs and produce outputs that no one can trust or audit.

Gartner projects that through 2026, 60% of AI projects will be abandoned specifically because organizations lack AI-ready data governance (Gartner, 2025).

9. Security Vulnerabilities and Adversarial Risk

AI models in insurance are targets. Adversarial attacks, where bad actors feed manipulated data to exploit model weaknesses, represent a growing threat. From inflated claim photos to synthetic identity fraud, the attack surface expands with every AI touchpoint. Insurers must implement model validation, input sanitization, and adversarial testing as standard practice.

Carriers working on AI-powered fraud detection in hospitals face particularly acute adversarial risks where manipulated billing data can compromise entire claim pipelines.

10. No Ethical Framework or AI Governance Board

AI in insurance makes decisions that affect people's financial security, health coverage, and property protection. Deploying AI without an ethical framework, including an AI governance board with cross-functional representation, creates blind spots. When something goes wrong (and it will), the absence of governance turns a fixable error into a crisis.

The Pain Is Real: What Failed AI Costs Your Organization

Failed AI projects do not simply waste budget. They create compounding damage across the organization:

- Financial loss: The average abandoned AI proof-of-concept consumes 6 to 12 months of team effort and hundreds of thousands in direct costs

- Talent attrition: Data scientists and engineers leave organizations where projects never reach production

- Competitive disadvantage: While you restart, competitors who got it right are automating underwriting, accelerating claims, and winning market share

- Regulatory exposure: AI models deployed without proper governance face enforcement action under emerging state and federal regulations

- Trust erosion: After one or two failed AI projects, executive teams become skeptical of future digital transformation investments

Is your AI investment delivering results, or draining resources?

Visit InsurNest to learn how we help insurers move AI from pilot to production.

Questions Insurance Leaders Ask About AI Failure

Before committing to another AI initiative, decision-makers need honest answers to hard questions:

- "Why did our last AI pilot fail to scale?" In most cases, the answer is not technology. It is data readiness, integration gaps, or change management failure.

- "How do we know if our data is AI-ready?" Conduct a data maturity assessment covering completeness, consistency, timeliness, and governance controls before selecting any AI vendor.

- "What should our realistic ROI timeline be?" Industry benchmarks indicate two to four years for meaningful AI returns, far longer than conventional IT payback periods of seven to twelve months (Risk & Insurance, 2025).

- "How do we protect against regulatory risk?" Implement explainability requirements, bias testing protocols, and audit trails aligned with NAIC guidance and state-level AI legislation.

- "Should we build or buy?" Most insurers lack the internal data science depth to build from scratch. Partnering with a specialist who understands insurance workflows, regulation, and integration reduces time-to-value significantly.

What Is the 4-Step Framework to Fix AI Failure in Insurance?

Insurers who succeed with AI follow a disciplined, phased approach rather than chasing technology trends. Here is the proven 4-step framework.

1. Assess Data Readiness and Define Clear Objectives

Before writing a single line of code, audit your data landscape. Map every source system, identify quality gaps, and establish data governance protocols. Simultaneously, define one to three measurable business objectives (such as "reduce claims leakage by 15%" or "cut policy issuance time by 50%").

| Assessment Area | Key Questions | Target Outcome |

|---|---|---|

| Data completeness | What percentage of fields are populated? | Over 95% field completion |

| Data consistency | Do formats match across systems? | Unified data dictionary |

| Integration architecture | Can systems share data in real time? | API-based data pipelines |

| Governance controls | Who owns data quality? | Assigned data stewards |

2. Start Small with a High-Impact Pilot

Select a use case with clear ROI potential, a manageable data scope, and executive sponsorship. Common high-impact starting points include AI-powered FNOL automation, claims triage, or underwriting document intake. Run the pilot for 90 days with predefined success metrics.

3. Invest Equally in People and Technology

Allocate budget for training, workflow redesign, and ongoing support alongside your technology investment. Create AI champions within each business unit. Establish feedback loops so frontline users can flag model errors and suggest improvements.

4. Scale with Governance and Continuous Monitoring

Once the pilot proves value, scale incrementally. Deploy model monitoring dashboards. Conduct quarterly bias audits. Maintain human-in-the-loop oversight for high-stakes decisions. Build your AI governance board with representatives from underwriting, claims, compliance, IT, and executive leadership.

| Phase | Duration | Activities |

|---|---|---|

| Data assessment and objective setting | 4 to 6 weeks | Data audit, KPI definition, vendor evaluation |

| Pilot deployment | 8 to 12 weeks | Single use case, controlled environment, daily metrics |

| Change management and training | Ongoing from week 1 | Role-based training, feedback collection, workflow updates |

| Scaled production rollout | 3 to 6 months post-pilot | Multi-use-case expansion, governance framework, monitoring |

| Total timeline to first production AI | 6 to 12 months | From assessment through scaled deployment |

Ready to move your AI from pilot to production?

Visit InsurNest to build an AI roadmap tailored to your insurance operations.

Why Should You Partner with InsurNest for Insurance AI?

InsurNest is built for insurance. We do not offer generic AI consulting repackaged for carriers. Our team combines deep insurance domain expertise with production-grade AI engineering, and every engagement is designed to deliver measurable outcomes.

What makes InsurNest different:

- Insurance-native AI solutions: Our models are trained on insurance-specific data patterns, not generic enterprise datasets

- Integration-first architecture: We build AI that connects to your existing policy admin, claims, and billing systems from day one

- Governance built in: Every solution includes explainability layers, bias monitoring, and regulatory compliance documentation

- Proven deployment methodology: We follow the 4-step framework above because we designed it through years of insurance AI delivery

- Post-deployment support: Our engagement does not end at go-live. We provide ongoing model monitoring, retraining, and optimization

Whether you need AI-powered underwriting automation or intelligent claims processing, InsurNest delivers AI that works in the real world of insurance.

The Urgency Is Now: Why 2026 Is the Tipping Point

The insurance AI landscape is shifting from experimentation to operational reliance. Industry AI spend is projected to grow by more than 25% in 2026 (Insurance Thought Leadership, 2026). Regulators are introducing AI examination tools. Competitors who solved these 10 failure points are already automating what your teams still do manually.

Every quarter of delay compounds the gap. The insurers who act now, with the right framework, the right data governance, and the right partner, will define the next decade of industry leadership.

The insurers who wait will spend the next decade catching up.

Do not let AI failure define your transformation story.

Visit InsurNest to start your AI success journey today.

Frequently Asked Questions

What percentage of insurance AI projects actually fail before reaching production?

Over 80% fail across industries per RAND Corporation 2025; only 22% of insurers reached full production per AllAboutAI 2026.

What budget should a CTO set aside for change management alongside AI spend?

Dollar-for-dollar match: spend equal amounts on change management and technology per McKinsey 2025 insurance research.

How long until our insurance AI investment delivers measurable ROI?

Two to four years for enterprise-wide returns versus 7 to 12 months for conventional IT per Risk & Insurance 2025.

Should my company build insurance AI in-house or partner with a specialist?

Partner. Only 7% of insurers have scaled AI internally; specialist vendors cut time-to-value significantly per BCG 2025.

What data readiness steps prevent AI failure before we start?

Audit completeness, standardize formats, assign data stewards, and build API pipelines; 60% of failures trace to data per Gartner 2025.

How does Colorado's AI Act affect our insurance AI deployment timeline?

Effective February 2026, it mandates impact assessments and consumer disclosures for high-risk AI decisions per Fenwick 2026.

What is the real cost when an insurance AI pilot fails to scale?

6 to 12 months of team effort lost, plus eroded executive trust that delays future digital transformation investment.

Does AI bias testing actually reduce regulatory risk for carriers?

Yes. NAIC model bulletins and Colorado's AI Act require documented bias testing; compliance prevents enforcement actions.

Sources

- Gartner: Lack of AI-Ready Data Puts AI Projects at Risk (2025)

- Insurance Business: Only 30% of Insurer AI Projects Make It Past Pilot Stage (2025)

- All About AI: AI in Insurance Statistics 2026

- Fenwick: Tracking the Evolution of AI Insurance Regulation (2026)

- Risk & Insurance: AI Investment Surges But ROI Questions Persist (2025)

- Wolters Kluwer: 2025 Insurance Tech Trends (2025)

- IQVIA: Model Bias and Governance in Healthcare Insurance (2025)

- Insurance Thought Leadership: 2026 The Year AI Goes Operational (2026)

- Informatica: The Surprising Reason Most AI Projects Fail (2025)

- Deloitte: Scaling Gen AI in Insurance (2025)